dTRINITY V1 Review & Intro to V2

- Jan 2

- 25 min read

Updated: Jan 26

1. Background

In December 2024, dTRINITY launched on Fraxtal, introducing the world’s first stablecoin protocol that pays interest rebates to borrowers. Since then, dTRINITY also expanded to Sonic and Katana, with protocol TVL reaching a $7M ATH prior to the recent market downturn.

One year in, dTRINITY’s borrower-subsidized stablecoin model has moved beyond theory and into reality. What began as an experiment is now a live, battle-tested DeFi primitive shaped by real users, liquidity, and market cycles. This report reflects on dTRINITY’s first year in production as 2025 comes to a close: how the protocol evolved, what worked well, what fell short, and how those lessons form the foundation for dTRINITY V2 in 2026.

2. V1 Overview

Microeconomics

From a microeconomic standpoint, dTRINITY is designed to stimulate onchain credit expansion by actively subsidizing stablecoin borrowers with interest rebates, funded by the stablecoin’s exogenous reserve earnings (float revenue). Subsidized loans increase credit demand and utilization, which raises lender yields. Higher yields then attract more capital to the protocol, expanding reserves and credit supply, further reinforcing float revenue and borrower subsidies to sustain growth.

In other words, dTRINITY subsidizes the demand curve and shifts it upward to establish a higher equilibrium of supply and demand, creating the following dynamics:

Because borrowers respond rationally to incentives, subsidies accelerate credit demand and push lending markets toward optimal utilization more efficiently than unsubsidized markets. At low utilization, subsidies lower the Net Borrow APY, enabling below-market borrowing rates. As utilization rises, dynamic DeFi interest rate models increase the Gross Borrow APY organically, producing above-market lending yields, while rebates keep the Net Borrow APY competitive.

When utilization is low, subsidy concentration may occur due to fewer outstanding debts vs. available rebates, which increases the marginal benefit of subsidies, potentially resulting in net negative interest rates, where users are effectively paid to borrow. Conversely, at high utilization, subsidy dilution reduces per-unit rebates and marginal benefit, raising the Net Borrow APY while naturally discouraging excess leverage until utilization returns to optimal levels.

The chart below illustrates the effect of borrower subsidies on a hypothetical dynamic interest rate model. The x-axis represents credit utilization, and the y-axis represents the net borrowing cost, with optimal utilization set at 90%. Due to subsidy concentration, the net borrowing rate becomes exponentially negative as utilization declines toward zero. This creates a powerful economic incentive that naturally attracts borrowers to sustain utilization around 90% or more, which is where the effect of interest rebates starts to become marginal as subsidized rates converge with market rates.

Macroeconomics

From a macroeconomic standpoint, dTRINITY’s borrower-subsidized stablecoin model increases aggregate onchain economic activity by activating yield-bearing capital that would otherwise remain underutilized in credit markets. Yieldcoins, for example, have very high borrowing costs that make them unsuitable to redeploy as lending liquidity (medium of credit).

By tokenizing idle yieldcoins, dTRINITY gains reserves to issue its own stablecoin, as well as float revenue to fund interest rebates. The newly issued stablecoin is not yield-bearing, allowing it to function more effectively as a medium of credit. Meanwhile, rebates subsidize the stablecoin’s net borrowing costs, making it cheaper to borrow than traditional, unsubsidized stablecoin loans. This process expands aggregate onchain credit supply and demand simultaneously.

Although yieldcoins can be used as collateral to borrow traditional stablecoins such as USDC, which technically increases aggregate credit demand, USDC must exist as a separate medium of credit with its own reserve backing. dTRINITY removes this constraint via its “yieldcoin-backed stablecoin,” allowing previously idle yieldcoins to be redeployed in a more capital-efficient form that could also earn lending yield, minimizing opportunity costs. As a result, dTRINITY helps the onchain economy access untapped credit capacity from existing yield-bearing capital, rather than relying on more stablecoin inflows to increase the aggregate credit supply.

Protocol Components

dTRINITY draws inspiration from Frax Finance’s DeFi Trinity framework to structure its protocol components around three distinct but interdependent functions: stablecoin, credit, and liquidity.

Stablecoin — The Decentralized Currency

At the core of dTRINITY is dUSD, an ERC20 stablecoin that serves as the protocol-issued unit of account, unifying liquidity between DEX pools and lending markets. It is backed 1:1 by onchain reserves composed of stablecoins and yieldcoins (e.g., frxUSD, sfrxUSD, DAI, sDAI). dUSD is soft-pegged to the US Dollar, with price stability maintained through open issuance/redemption, natural market arbitrage activity, and protocol buybacks when necessary. Users may mint or redeem dUSD atomically using whitelisted reserve assets.

Lending Protocols — Onchain Credit Engines

To earn lending yield, users may stake dUSD into the protocol’s ERC4626 vault to mint sdUSD, the yieldcoin version of dUSD — introduced in August 2025. Deposited assets are automatically supplied into dTRINITY’s multi-collateral lending protocol, dLEND (an Aave V3 fork), generating yield for sdUSD holders.

sdUSD can be staked or unstaked atomically, subject to available liquidity in dLEND. As a liquid and composable lending vault token, sdUSD can be used in the broader DeFi ecosystem to unlock more utility and capital efficiency, such as providing liquidity on DEXs. Users who prefer to lend directly may instead supply dUSD into dLEND or strategic lending protocol partners. However, direct lenders do not receive the sdUSD vault token.

Once lenders have added credit supply, borrowers can then deposit collateral into dLEND to access dUSD loans from whitelisted markets. While borrowers still pay a Gross Borrow APY, they earn an additional Rebate APY (paid in dUSD) based on the size of their outstanding debts. These interest rebates are continuously funded by dUSD float revenue, providing an exogenous and renewable source of yield to subsidize borrowers’ net costs.

Note: dUSD is the only stablecoin that users can borrow in dLEND. It is also disabled as a collateral to secure loans across all integrated markets to prevent recursive subsidy arbitrage (subsidy looping).

DEXs — Onchain Liquidity Pools

Robust credit requires deep secondary market liquidity, as borrowed stablecoins are typically sold to access leverage. In dTRINITY’s case, low DEX liquidity would push borrowers to redeem dUSD, which leads to reserve contraction and subsidy dilution, marginalizing the effectiveness of interest rebates. To scale, credit demand should be accompanied by LP demand to bolster DEX liquidity and divert redemption pressures from borrowers.

dTRINITY integrates with top stablecoin-centric DEXs like Curve Finance to facilitate onchain trading and liquidity for protocol-issued assets. Users can swap efficiently between dUSD, sdUSD, and other tokens, while LPs and market makers can earn pool trading fees, farm incentive rewards, and capture arbitrage opportunities.

Curve LP incentives for dUSD and sdUSD pools are supported by a mix of protocol revenue, early project funding (pre-TGE), and token emissions (post-TGE), potentially amplified through Curve’s veTokenomics mechanism. As dTRINITY scales, subsidized credit expansion is expected to drive higher money velocity, volume, and fees, organically enhancing LP returns while gradually reducing reliance on protocol incentives.

Dual-Incentives — Subsidies & Emissions

In the future, dTRINITY plans to launch a token generation event (TGE) for its governance token, TRIN. While initially targeted for the end of 2025, the timeline has been revised in light of recent market events as well as community feedback. The TGE for TRIN is now set to take place in 2026, allowing extra time for protocol maturation and improved market conditions. More details regarding the TGE, tokenomics, and governance will be released in Q2 2026.

Prior to the TGE, lenders and LPs will continue earning dT Points, which convert into TRIN tokens during the TGE. The dT Points Program is designed to align early participants with the protocol’s long-term growth and sustainability. Post-TGE, TRIN will enable decentralized governance of dTRINITY through a model similar to Curve’s veCRV. Vote-escrowed users, or veTRIN holders, will govern key protocol decisions, including reserve allocations, collateral whitelisting, incentive allocations, open market operations, and core protocol parameters.

Under dTRINITY’s dual-incentive system, exogenously funded dUSD interest rebates subsidize borrowers (demand), while endogenous emissions of TRIN tokens or dT Points reward lenders and LPs (supply), on top of native yields. veTRIN holders may one day vote to decide how these incentives are spent across internal and external markets for protocol-issued assets.

Over time, TRIN is expected to accrue governance demand as external protocols compete for veTRIN votes to influence incentive flows toward their markets that support dTRINITY’s assets. Marketplaces for buying and selling veTRIN votes should also emerge naturally, unlocking a new source of yield for veTRIN. In theory, the system may converge toward a competitive equilibrium in which TRIN’s value could be priced partially by the marginal economic impact of the incentive capital controlled through governance. In other words, TRIN’s valuation may be determined by, among other factors, the discounted value of its influence over future incentive allocations and the incremental economic outcomes created by those incentives.

3. Why dTRINITY?

dTRINITY addresses three structural problems facing the stablecoin and onchain lending industries today: float revenue capture, supply centricity, and capital inefficiency. These problems originate from the concentration of value at the token issuer level and among passive supply-side participants. With dTRINITY, incentives are restructured to improve capital efficiency and credit demand, aligning value creation and distribution on both sides of the market.

Float Revenue Capture

Stablecoin float revenuegenerated by issuers worldwide has surpassed $10 billion annually, mostly dominated by Tether (USDT) and Circle (USDC). This revenue is largely earned from reserves held in short-term US government bonds, bank deposits, and cash equivalents. However, a majority of the float revenue is internalized by stablecoin issuers, creating a disparity in economic benefit between issuers and users.

dTRINITY realigns incentives by distributing dUSD’s float revenue to protocol users, transforming passive reserve earnings into an active mechanism to stimulate onchain credit formation, economic activity, and ecosystem growth.

Supply Centricity

Supply centricityrefers to the traditional yield distribution model used by most stablecoin and yieldcoin projects, where yield is shared with token holders or liquid stakers. While this approach rewards passive capital accumulation, it does not create credit demand for this capital. In fact, yieldcoins are expensive mediums of credit because supply-side yield accrual compounds interest expense for yieldcoin borrowers, on top of standard borrowing costs. dTRINITY, on the other hand, takes a demand-centric approach, where float revenue is repurposed as subsidies to lower net interest expenses and increase credit demand, naturally unlocking higher yield for lenders.

Like Yin and Yang, dTRINITY’s demand-centric model introduces the long-missing counterpart to current supply-centric models, completing the feedback loop between stablecoins, credit, and liquidity within decentralized markets.

Capital Inefficiency

Capital inefficiency is most apparent in DeFi lending protocols, where yieldcoins are primarily supplied as collateral rather than as lending liquidity. This is a structural side effect caused by supply-centric models. As a result, borrowers tend to avoid them as a medium of credit, leaving yieldcoin supplies mostly idle.

To make yieldcoins capital efficient, dTRINITY turns them into reserves and issues a borrower-friendly stablecoin that redirects float revenue toward subsidizing loans instead of compounding their costs. Previously idle yieldcoin holders can now redeploy their capital productively, substituting native yield with enhanced lending yield.

Traditional stablecoin deposits in lending protocols also suffer from capital inefficiency during prolonged periods of credit contraction, when utilization may fall below optimal levels. Since most stablecoin issuers either hoard float revenue or rely on supply-centric yield distribution mechanisms, borrower support is often neglected. When borrowers do receive incentives, they are usually based in points or endogenous token emissions, which are less desirable and not long-term sustainable.

In contrast, dTRINITY’s borrower subsidies model is designed to sustain credit demand and capital efficiency through all market cycles. Even as float revenue and interest rebates decline during low-yield environments, reduced subsidies still provide materially better outcomes vs. no subsidies. As a result, dUSD can sustain a higher long-run equilibrium of utilization and capital efficiency than unsubsidized stablecoins.

4. Risk Management

There are five key sources of risk to dTRINITY users: security risk, stablecoin reserve risk, lending collateral risk, oracle risk, and liquidity risk. User safety is prioritized through prudent system design, asset curation, code audits, and ongoing risk management by the core team.

Security Risk

Securityis one of the most common risk vectors in DeFi which is why regular internal and external code audits form the security backbone of dTRINITY. Since inception, the protocol has completed nearly $200,000 worth of audits with five independent Web3 security firms: Verichains, Cyberscope, Halborn, Hats Finance (public competition), and most recently Hashlock, with more third-party engagements and audit competitions planned in 2026. In parallel, the dTRINITY team actively employs proprietary AI-powered auditing tools and the Hypernative Security Oracle to review and monitor smart contracts for potential vulnerabilities. Core team members also follow strict OpSec and multisig key management practices to minimize risk and strengthen governance safety.

Stablecoin Reserve Risk

Stablecoin reserves form the economic backbone of dTRINITY, underpinning most protocol participants. Therefore, reserve assets must be carefully curated and whitelisted based on their collateral, liquidity, track record, and risk profile. For each chain dTRINITY expands to, only the top qualified assets in that ecosystem may be accepted into the protocol’s reserve. Additionally, reserves are chain-isolated by design, intentionally sacrificing dUSD’s cross-chain fungibility to contain risk from chain-specific events. A portion of protocol revenue is also retained to over-collateralize reserves, building a risk buffer over time. In the event that the reserve becomes under-collateralized, redemptions may be paused temporarily to protect users and support the re-collateralization process.

Lending Collateral Risk

Lending collateral secures outstanding debt which is vital to the health of dUSD lenders (and sdUSD holders). Similar to stablecoin reserves, collateral support is strategically curated for dUSD markets in dLEND and other integrated lending protocols. Unproven or low-liquidity assets are generally avoided, reducing the risk of extending credit against unsafe collateral. Furthermore, the maximum loan-to-value (LTV) ratio for dLEND markets is capped at 80% (with liquidation at 85%), limiting borrowers to at most 5X leverage. Collateral rehypothecation also disabled in dLEND by default to mitigate nested leverage and cascading liquidation. Ultimately, these measures help lower bad debt risk, prioritizing lender safety over borrower flexibility.

Oracle Risk

Oraclescarry risk when price feeds become inaccurate, delayed, or manipulated, potentially impacting protocol operations and user positions. To mitigate this, dTRINITY integrates with multiple oracle providers, including Api3, RedStone, and Chainlink, with additional sources planned in the future to improve redundancy and reliability.

For minting/redeeming, staking/unstaking, and lending/borrowing transactions, dUSD’s price is hard-coded at $1 to prevent potential market manipulations and encourage arbitrageurs to stabilize the peg. Since dUSD only functions as a debt asset in lending markets, not as collateral, hard-coding its price minimizes oracle-related risk without affecting lending operations for dUSD.

A majority of yield-bearing reserve and collateral assets are priced based on the unit NAV (net asset value) of their underlying holdings rather than market-traded prices. This reduces exposure to dislocations caused by temporary liquidity issues. Where applicable, composite pricing is used (e.g., sfrxUSD/frxUSD x frxUSD/USD) to obtain prices based on fundamental backing. Furthermore, if a stablecoin feed such as frxUSD/USD reports a price above $1, which is likely to be a temporary anomaly, the dUSD minting contract will round it down to $1, preventing mints from posing under-collateralization risk.

Liquidity Risk

Liquidity is critical to maintaining the soft pegs of protocol-issued assets and enabling low-slippage trading on DEXs. dTRINITY supports this through atomic, permissionless issuance/redemption and staking/unstaking, allowing arbitrageurs to facilitate the price discovery and peg-keeping process. If dUSD trades at a significant discount, the protocol may execute a Stability Market Operation (SMO) to buy back dUSD using reserves, restoring DEX liquidity and price stability while capturing arbitrage revenue.

dUSD lenders and sdUSD users also require unutilized liquidity to either exit or perform arbitrage. If borrower subsidies push credit utilization above optimal levels, sdUSD may start trading below its underlying value as users may be forced to sell instead of unstaking. In this case, the protocol can increase the Net Borrow APY by tapering rebates to encourage repayments and restore lender liquidity.

Disclaimer: The risks described above are not exhaustive. Additional material risks may include, but are not limited to network risk, governance risk, leverage risk, and market volatility. The protocol aims to manage and mitigate these risks, though they cannot be eliminated entirely. Users should conduct their own due diligence to fully understand the risks involved, including the potential loss of funds. For more information, please refer to the Full Disclaimer.

5. V1 Performance

Achievements

Since launching in December 2024, dTRINITY has successfully validated its DeFi primitive in production. The protocol demonstrated that demand-centric subsidies can shift stablecoin lending markets toward a stronger equilibrium, with better capital efficiency and credit demand. This is showcased through dTRINITY’s deployment on Fraxtal, its genesis network.

High Credit Utilization

dLEND achieved 84.7% average daily utilization vs. 78.3% for Aave USDC, outperforming Aave on 70% of days throughout 2025. This confirms that borrower subsidies structurally anchor credit demand around target utilization.

Below-Market Borrowing Rates

A majority of Fraxtal dUSD’s reserve is allocated into bridged sDAI from Sky and sfrxUSD, the leading native yieldcoin from Frax. Float revenue from the reserve funded borrower subsidies, allowing dLEND dUSD users to access below-market rates about 73% of the time, with an average daily Net Borrow APY of 2.9% — half of Aave USDC’s 5.9%. In total, dTRINITY distributed more than $51,000 in dUSD rebates on Fraxtal over a year, funded by yield-generating reserves that averaged $648,000 daily, or 7.9% APY in float revenue. These rebates subsidized $815,000 in outstanding loans on average, implying a daily Rebate APY of 6.3% and a Debt-to-Reserve ratio of 1.25, which measures credit expansion relative to reserves.

Above-Market Lending Rates

High utilization translated directly into superior yields, with dUSD lendersearning more than stablecoin market rates about 91% of the time, capturing an average daily Supply APY of 7.9% — an 88% outperformance vs. Aave USDC’s 4.2%. In addition, borrower subsidies enabled dLEND dUSD to consistently deliver a higher Supply APY than its Net Borrow APY, a rarely seen phenomenon in traditional markets, where borrowing rates are almost always higher than lending rates.

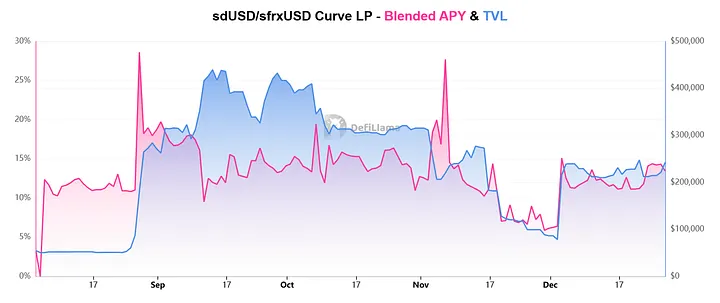

Competitive LP Yields

At the moment, dTRINITY relies on non-float protocol revenue and early project funding to incentivize its Curve liquidity pools on Fraxtal, focusing on dUSD/frxUSD (stablecoin pool) and sdUSD/sfrxUSD (yieldcoin pool). Incentives are deployed through Curve’s veTokenomics mechanism, unlocking CRV token emissions to LPs. Frax co-incentives for LPs may also be available via WFRAX token emissions.

Historically, dUSD and sdUSD pools generated blended LP APYs between 10–20%, inclusive of trading fees, token incentives, and/or native yields from pool assets. The sdUSD/sfrxUSD pool, in particular, ranked among Curve’s top three yielding pools during the weeks of August 28 and September 11, driven mainly by native yields with CRV emissions layered on top.

Curve LPs also helped absorb selling pressures from dUSD borrowers, diverting them from direct redemptions, which otherwise would lead to reserve contraction and, subsequently, rebate tapering. Thanks to healthy Curve incentives and liquidity, the protocol was able to maintain a low Debt-to-Reserve ratio, enabling sustained expansion while preserving reserve efficiency and consistent borrower subsidies for dUSD.

Peg Stability

During its first 30 weeks, dTRINITY experimented with a no-redemption policy, relying mainly on SMOs as the peg stabilization mechanism for dUSD. The experiment’s objective was to assess the effectiveness of protocol buybacks since users could not redeem dUSD directly to perform arbitrage. The following observations were made from the experiment:

During credit expansion cycles, selling pressure from borrowers caused dUSD to trade at a discount as Curve pools accumulated more dUSD relative to other paired assets. During credit contraction cycles, borrowers bought back dUSD to unwind debt, rebalancing the pools and pushing dUSD back toward $1.

When dUSD traded at a significant discount between $0.975 and $0.99, SMOs were executed through the dUSD/frxUSD pool to repurchase and redeem dUSD. In total, 10 SMOs were successfully conducted between December 20, 2024 and July 31, 2025, each time restoring dUSD to a range between $0.995 and $1.

SMOs often marked the end of a credit expansion cycle, shortly after the largest wave of borrowers sold dUSD. SMOs also caused reserve contraction and reduced float revenue, leading the protocol to taper rebates periodically, as intended. This increased dUSD’s net borrowing costs, which triggered credit contraction cycles, periods when dUSD began trading closer to $1 organically.

While SMOs demonstrated their ability to stabilize dUSD’s peg, fewer market participants engaged in “front-running” SMOs than anticipated, resulting in higher peg volatility during credit expansion cycles. As a result, the experiment was ended and atomic redemption was enabled on August 4, allowing users to arbitrage dUSD more effectively. Since then, no additional SMOs were needed.

The protocol applies a redemption fee of up to 0.5% on dUSD to generate revenue and fund incentives. As a result, market participants bake in this fee as a price discount, which means dUSD now tends to hover around $0.995. Deeper price discounts often get arbitraged quickly as it becomes profitable to do so.

In early November, dUSD briefly fell below $0.97 on Fraxtal due to contagion fears stemming from the Sonic Incident (see page 13 for more details). However, there was no impact to the protocol on Fraxtal, which is isolated from the Sonic network by design. Arbitrageurs quickly realized this and restored dUSD’s price to above $0.995, aided by the availability of atomic redemption.

Chain Expansions

dTRINITY has completed deployments on three blockchains: Fraxtal, Sonic, and Katana. These emerging ecosystems serve as the protocol’s early beachhead markets, allowing it to validate core assumptions, live performance, and growth strategies prior to expansions on Ethereum and other major networks. Each deployment maintains fully chain-isolated reserves and collateral for dUSD, sdUSD, and dLEND. As a result, protocol-issued assets share similar names but they are not fungible cross-chain.

Fraxtal: A stablecoin-focused layer-2 blockchain developed by Frax, launched in February 2024. Fraxtal is the genesis network of dTRINITY, where all protocol components were deployed alongside Curve liquidity pools in December 2024. Frax is also a key partner of dTRINITY, supporting the project with strategic advice, grants, liquidity, and ecosystem incentives, including FXTL Points allocated to its users on Fraxtal.

Sonic: A DeFi-focused layer-1 blockchain (fka Fantom), launched in December 2024. Sonic was the first chain expansion of dTRINITY following its genesis on Fraxtal. The protocol launched on Sonic in May 2025 with all core components deployed. Subsidized lending markets were activated in both dLEND and Silo, the first externally integrated lending protocol where borrowers can also earn interest rebates on dUSD loans (distributed via Merkl). Additionally, liquidity pools for protocol-issued assets were created on Curve as well as Beets and SwapX.

Katana: A DeFi-focused layer-2 blockchain incubated by Polygon Labs and GSR, launched in July 2025. dUSD was deployed on Katana in October as a standalone protocol component, allowing dTRINITY to prioritize collaborations with Yearn on risk-curated vaults and Morpho on subsidized lending markets, where borrowers can earn interest rebates on dUSD loans (distributed via Merkl). Liquidity pools for dUSD are also available on Sushi Swap. Additionally, KAT Points are rewarded to dUSD users on Katana as ecosystem incentives, initially to LPs.

Strategic Partnerships:

Since inception, dTRINITY has secured multiple collaborations and integrations with leading DeFi protocols to expand reach, distribution, and leverage symbiotic growth opportunities through shared users, such as:

Collaborating with stablecoin and yieldcoin issuers to support their assets as reserves, collateral, or liquidity, enabling new markets and strategies for users. These protocols can mutually integrate sdUSD as yield-bearing reserves, collateral, or liquidity within their ecosystems as well.

Collaborating with lending protocols and incentive protocols to enable external dUSD lending markets and distribute borrower subsidies, respectively.

Collaborating with DEXs and liquidity aggregators to enhance trading efficiency and enable incentivized liquidity pools for dUSD and sdUSD.

Collaborating with vault protocols to enable unique strategy vaults for dUSD and sdUSD, improving user experience and potential performance.

Collaborating with derivative protocols like interest rate marketplaces to enable yield trading for sdUSD through principal tokens (PT) and yield tokens (YT).

A table of the protocol’s partners is provided below for reference. Additional partnerships and integrations are planned over time, including categories that have not been listed.

Battle-Tested Security:

To date, dTRINITY has experienced zero end-user losses from security incidents. However, a vulnerability was uncovered during the Swap Adapter Incident in August, which led to limited losses affecting three core team members. The issue was immediately addressed and no user funds were impacted, though the incident provided a valuable lesson in improving protocol security and auditing processes (more details on pages 14 and 16). No other security incidents took place since inception.

Shortfalls

While the core economic thesis proved sound, dTRINITY V1 also exposed several shortfalls. These issues do not stem from the borrower-subsidized stablecoin model itself, but signals of where better protocol designs and risk management are required.

Sonic Incident

In May, dTRINITY expanded to Sonic in response to its strong ecosystem momentum at the time, growing to over $1B in TVL within the previous six months. Unlike its deployments on Fraxtal and Katana networks, dTRINITY did not secure a strategic partnership with Sonic, which is why Sonic Points were not allocated to dTRINITY users as ecosystem incentives. In contrast, Fraxtal and Katana both support dTRINITY users with FXTL Points and KAT Points, respectively.

As with every chain deployment, dTRINITY followed its standard risk framework by selectively whitelisting the most established Sonic-native assets for the protocol’s reserve and collateral. Sonic USD (scUSD) and Staked Sonic USD (wstkscUSD) were included under this framework, as they are the de-facto ecosystem stablecoin and yieldcoin issued by Trevee Earn (fka Rings Protocol). These tokens were also among the largest native assets at the time, with active Sonic Points allocated to their users.

In early November, the sudden collapse of Stream Finance’s xUSD, an external yieldcoin that made up more than half of Sonic’s total yieldcoin supply, triggered severe ecosystem-wide contagion. Trevee was directly impacted due to its exposure to xUSD through an Eulerlending vault curated by MEV Capital, which led to rapid devaluation of wstkscUSD and downstream impairments on dTRINITY’s Sonic deployment. Fortunately, dTRINITY’s deployments on Fraxtal and Katana remained unaffected thanks to the protocol’s chain-isolated reserves and collateral design, fully containing the contagion within its Sonic deployment.

Following the incident, Sonic dUSD de-pegged significantly and the protocol incurred bad debt for dLEND dUSD and sdUSD holders on Sonic, impacting both end users and the core team’s capital. The Sonic deployment has since been paused, pending ongoing legal recovery efforts by Trevee from Stream Finance. Further expansions on Sonic are also halted for the time being to prioritize re-collateralization.

To aid recovery efforts, the core team has committed to donating 100% of its claims toward supporting impacted dTRINITY users on Sonic, potentially eliminating reserve under-collateralization and reducing net bad debt to less than $50,000 if wstkscUSD is able to recover to at least ¢0.30 on the dollar. For more details, please refer to the post-mortem.

Swap Adapter Incident

In August, Hypernative alerted that dLEND experienced a swap adapter attack, where only core team members were affected. The exploit stemmed from a vulnerability in an ODOS adapter contract that allowed arbitrary callers to spend previously granted unlimited approvals, which was missed during a prior third-party audit engagement. In total, $56,000 was drained from three engineers’ personal wallets which had granted unlimited approvals during testing and development. No external user funds were lost since the protocol does not set user transactions to have unlimited approvals by default.

Upon discovery, the exploited feature was promptly removed from the protocol’s interface and users were quickly notified to revoke approvals where necessary. Mitigation steps were also implemented, including additional security improvements, smart contract audits, and refunds for the engineers. For more details, please refer to the post-mortem.

Neglecting Supply

dTRINITY is designed to be demand-centric, based on the thesis that stronger credit demand ultimately benefits both sides of the market. In practice, this takes time to happen organically at scale. Borrower subsidies can only activate once lender capital is present to expand reserves, fund subsidies via float revenue, and supply credit. Without consistent lender inflows, credit expansion is limited by available reserves and lending deposits (a classic chicken-and-egg problem).

Although dUSD lenders earn competitive yields, including dT Points, these incentives alone have not been sufficient to rapidly mobilize lender inflows. For newer protocols such as dTRINITY, lenders may demand returns three to five times above prevailing market rates to compensate for perceived risk. As a result, additional supply-side incentives, effectively lender subsidies, may be needed to further accelerate dTRINITY’s flywheel until critical mass and credibility are achieved.

Lessons Learned

Note: Protocol TVL includes dUSD’s reserves, pre-minted dUSD, staked dUSD, and dLEND deposits.

dTRINITY’s achievements and shortfalls during its first year provided valuable insight into how the protocol performed under live market conditions. These experiences highlighted which design choices proved effective and which areas need refinement as the system matures. The lessons learned in 2025 will directly inform the design and evolution of dTRINITY V2 in 2026.

Subsidized Credit Demand

Borrower subsidies performed as intended, validating dTRINITY’s unique model in production. Therefore, the protocol will continue distributing float revenue as demand-side incentives to dUSD borrowers.

Redemption & Stability

To enhance peg stability and arbitrage participation, dTRINITY will permanently enable atomic redemption for dUSD, unless there is an emergency that requires closing redemptions temporarily. The protocol will also continue executing SMO buybacks strategically if dUSD trades at a significant discount. However, fewer protocol interventions are expected in the future as long as redemptions are available. Moreover, dUSD redemption fees may be reduced to decrease peg volatility during credit expansion cycles.

Chain Expansions & Isolation

In 2026, dTRINITY will focus chain expansion efforts mainly on Ethereum and leading layer-2 networks like Base and Arbitrum where DeFi ecosystems are mature, with more collateral diversity and potentially less systemic risk. Protocol reserves and collateral will continue to be isolated per chain, a design choice validated through the Sonic Incident.

Reserve & Collateral

dTRINITY V2 will adopt a stricter framework for curating reserve and collateral assets. Going forward, only a limited set of eligible assets from leading projects with proven track records will be incorporated into dUSD’s reserves and/or dLEND’s collateral pools (more details in Section 6). Beyond curation, active monitoring and pre-emptive measures may be taken by dTRINITY to reduce exposure to, or replace, any asset that presents heightened risk to the protocol.

Protocol Security

After the Swap Adapter Incident, dTRINITY engaged Hashlock to conduct a new round of smart contract audits, with heightened focus on the component where vulnerabilities were identified. The core team is also leveraging recent advances in AI to support ongoing internal audits, including invariant testing, complementing manual reviews from dedicated security personnel. These AI-powered tools are expected to improve audit scalability and efficiency over time. In addition, automated threat detection and prevention features from Hypernative are being evaluated to enhance real-time and pre-emptive response capabilities. Looking ahead, the protocol will continue to strengthen its security with regular audits, bug bounties, active monitoring to mitigate risk.

Balancing Incentives

Although supply-side incentives are necessary to attract more lender inflows, they should not dilute borrower subsidies or LP incentives. dTRINITY V2 will address this through a new mechanism to increase reserve efficiency, market liquidity, and float revenue, with only limited incremental risk (more details in Section 6).

6. V2 Enhancements

Drawing from its lessons in 2025, dTRINITY V2 introduces new upgrades to strengthen supply-side participation, deepen liquidity, and tighten asset curation, positioning the protocol for better long-term growth and resiliency. Much of this groundwork is already underway on Fraxtal, with a full V2 deployment and an official expansion to Ethereum scheduled in January 2026.

Algorithmic Market Operations (AMO)

Although DEX AMOs were part of dTRINITY V1’s original design, they were never fully deployed due to competing priorities. The AMO contracts have since been finalized, audited, and are now ready for implementation in V2.

Also known as direct deposit modules, AMOs were originally pioneered by Frax in 2022. They enable onchain market operations where stablecoins are “pre-minted” to provide liquidity in DEXs or lending markets without causing significant price discounts. Pre-minted tokens are effectively backed by themselves since they remain on both sides of the protocol’s balance sheet until entering circulation via swaps or lending activity. Therefore, AMO positions are considered part of the protocol’s reserves.

dTRINITY V2 only supports DEX AMOs deployed on Curve. Pre-minted dUSD and sfrxUSD from the reserve currently make up its AMO position on Fraxtal via the dUSD/sfrxUSD Curve pool. The Curve AMO distributes pre-minted dUSD at a near 1:1 rate (in dollar terms, accounted for fees and slippage) when users swap sfrxUSD into the pool, thereby collateralizing previously unbacked supply upon entering circulation. Conversely, users can swap circulating dUSD into the pool in exchange for sfrxUSD from the Curve AMO, returning it to a pre-minted state.

Curve AMOs enable dTRINITY V2 to enhance peg stability, capital efficiency, and float revenue, unlocking greater liquidity and incentive funding for protocol users.

Peg stability may be influenced via AMOs by injecting pre-minted liquidity into Curve pools when dUSD supply is too low (price premiums), or removing pre-minted liquidity from Curve pools when dUSD supply is too high (price discounts). The protocol may also capture arbitrage P&L from this AMO rebalancing process.

Capital efficiency increases significantly by leveraging existing reserves and pre-minted dUSD to bootstrap DEX liquidity and protocol TVL. Similar to LPs, the AMO also earns trading fees and CRV token emissions through Curve’s veTokenomics mechanism. Pre-minted liquidity could potentially amplify these AMO earnings, further boosting reserve productivity and yield generation.

Float revenue may increase through a combination of AMO yield farming and arbitrage P&L, providing extra incentive funding for protocol users. Similar to native yields from reserve assets, AMO earnings fluctuate based on market conditions. When yield farming is not profitable, the protocol may reduce its AMO activity until market conditions improve.

AMOs also introduce new risks, including but not limited to security. As such, the AMO contracts have undergone both internal and external audits by Hashlock prior to production, with more reviews and audits planned over time.

Beyond security risks, dUSD’s reserve integrity now becomes partially dependent on DEX operations. For this reason, dTRINITY’s AMOs are deployed exclusively on Curve, relying on its battle-tested infrastructure since 2020, where many other stablecoin protocols also deploy their AMOs (e.g., Frax, Origin, Inverse Finance). dTRINITY’s AMOs will not be deployed on networks where Curve is not available. Other established DEXs may be considered as AMO deployment venues in the future through protocol governance.

Adaptive Incentive Allocation

Adaptive incentive allocation refers to dTRINITY V2’s ability to periodically reallocate user incentives to where they are most effective. Float revenue generated from yield-bearing reserve assets and AMO earnings can be allocated to either the demand side (borrowers), the supply side (lenders), or both, depending on market conditions. When credit demand weakens, a greater share of incentives is directed toward borrowers to stimulate utilization. Conversely, when lender inflows are lagging, incentives can be shifted toward lenders to attract new reserves and credit supply, enabling further expansion. This approach can be applied to both subsidies and protocol emissions.

Supply-side incentives can be optimized by routing them through sdUSD liquidity pools on Curve rather than to dUSD lenders directly, since sdUSD holders and LPs are effectively dUSD lenders. By incentivizing sdUSD pools, LPs earn trading fees and CRV emissions on top of lending yield. dTRINITY may also leverage Curve’s veTokenomics mechanism to potentially amplify supply-side incentives, improving sdUSD liquidity while indirectly reinforcing dUSD stability via cross-market arbitrage. Together, this adaptive incentive framework allows dTRINITY V2 to influence supply and demand more efficiently, fully balancing Yin and Yang within its ecosystem.

Asset Curation Framework

Below are dTRINITY’s current criteria for whitelisting reserve and collateral assets. Changes to these criteria may be decided through protocol governance in the future.

Stablecoin & Yieldcoin Reserves: Only assets from the following established issuers and protocols may be included in dUSD’s reserves (subject to network availability):

Note: Aave deposits for reserve assets are included, allowing the reserve to hold stablecoin-denominated lending receipt tokens (aTokens).

Lending Collateral: dLEND’s collateral pools will only support assets from the above issuers, as well as assets already supported by Aave, the world’s largest lending protocol. Eligible assets may include crypto, yieldcoins, onchain bonds, liquid staking tokens (LST), liquid restaking tokens (LRT), Pendle PT assets, and tokenized real-world assets (RWA). This approach allows dLEND to mirror Aave’s risk curation standards, which extend to the sdUSD vault as well.

A table of currently supported and planned assets is provided below for reference. Additional assets that meet the above criteria may be whitelisted over time.

7. Roadmap for 2026

dTRINITY will prioritize the rollout of V2 and its expansion to Ethereum during the first half of 2026. In the second half of the year, the protocol plans to expand to Base and Arbitrum, launch the TRIN TGE, and progressively decentralize governance to veTRIN holders. New products, features, and markets for protocol-issued assets will be introduced throughout the year, while most strategic partnerships can be replicated and scaled across integrated networks, enabling a consistent product and growth blueprint wherever the protocol expands.

dTRINITY’s tentative roadmap for 2026 is provided below for reference. Please note that these plans are forward-looking and subject to change over time.

8. Final Thoughts

dTRINITY started with a simple but unconventional thesis: stablecoin float revenue should support credit demand, not just accrue to issuers or passive holders. After a full year in production, this thesis has been tested across real users, real capital, and live market conditions. The protocol’s achievements and shortfalls both provided valuable insight into how incentives, liquidity, and risk interact at scale. These lessons are embedded in dTRINITY V2 through more disciplined designs, enhanced mechanisms, and adaptive incentives to balance the forces of supply and demand. As the protocol enters 2026, the focus now changes from validating to scaling, expanding to networks with deeper liquidity and mature markets, where dTRINITY’s subsidized stablecoin model can realize its full potential.

“All things carry Yin and embrace Yang; they achieve harmony through balance” ~Lao Tzu ☯︎

📢 Join the dTRINITY community to get the latest updates!

Website | X (Twitter) | Documentation | Discord | Blog | Other links

Disclaimer: dTRINITY is not available to residents of Canada, Iran, North Korea, Russia, the USA, the UK, and other restricted regions.

The information contained herein should not be considered legal, business, financial, or tax advice. Past performance is not indicative of future results. Digital assets and DeFi protocols carry significant risks, including the potential for complete loss of funds. By using dTRINITY, you acknowledge and accept these inherent risks. View our full Disclaimer and Terms to learn more about the risks involved.